中文

中文Enthusiasm for Burgundy’s wines continues apparently unabated, as could be witnessed by attending the recent 17th Grands Jours de Burgundy event that ended on March 22. This year saw 2,391 professionals from 58 countries attend (37.7% of whom were new), representing a 3.5% increase compared to 2018 (the last “normal” edition before COVID). Importers, wine merchants, agents, sommeliers, restaurateurs and journalists discussed and tasted through the 2022 vintage with representatives of négoces, coop-cellars and estates from all over Burgundy.

Burgundy has finally been able to replenish its stocks with a second generous harvest in 2023. Periodic shortages of wine are one of the challenges affecting Burgundy’s development in its markets. The challenge now is to re-learn how to build up stocks for the coming years, while also seeking to renew our foothold in markets that are undergoing major changes, both in France and abroad.

The available stock in Burgundy, at the start of the 2023-2024 campaign, has been replenished by two generous back to back harvests, 2022 and 2023: wineries have an increase of 12% of available stock compared to the average of the last five years.

Burgundy has not seen a situation like this for over 20 years. This allows the industry to better anticipate potential future hazards and preserve its market share.

One of the challenges is to revive Burgundy’s development in the markets, which has been limited in recent years by lower productivity and its many consequences.

Bulk wine sales from estates are up compared to the same period in the previous campaign: +8% for the first six months of the 23-24 campaign compared to the first six months of the 22-23 Bulk wine accounts for 67.5% of total sales volumes (bulk + bottles), even though the pace of transactions is a bit slower than in the previous campaign.

In terms of exports, the markets are facing a number of uncertainties linked to the geopolitical situation, such as the upcoming United States election, as well as the continuing trend towards increasingly occasional consumption.

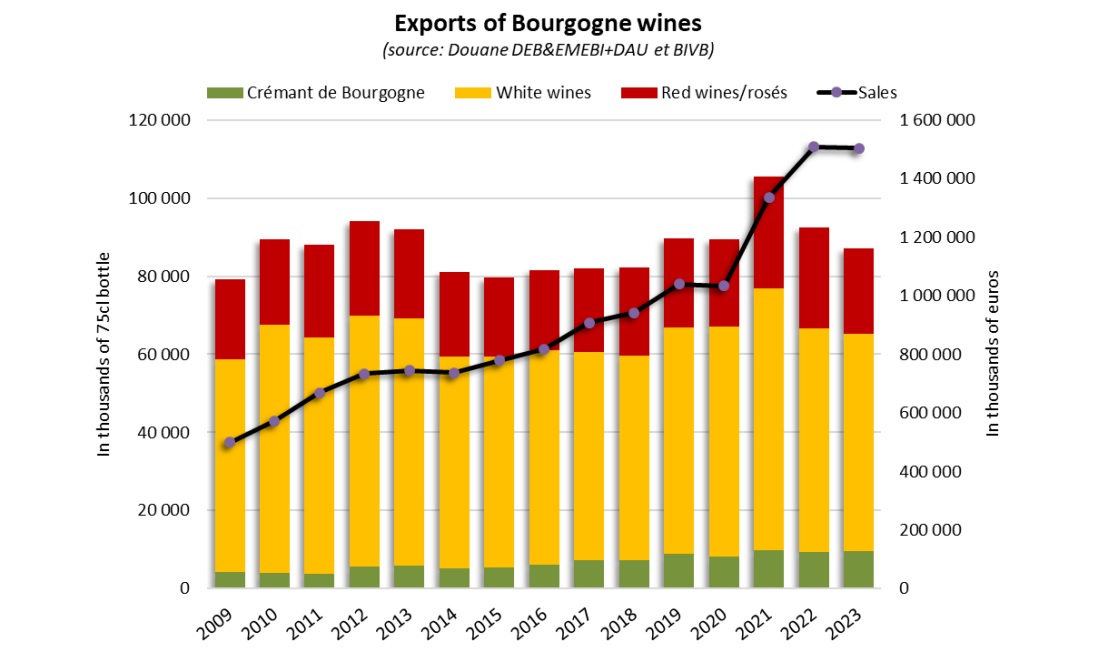

Burgundy exports felt the effects of this in 2023, with an export volume down 6% compared to 2022 (87 million bottles1). And while sales remained above one billion euros for the 4th consecutive year at 1.5 billion euros, that was down 0.3% compared to 2022.

- Burgundy is well aware of the many challenges it must confront: maintaining its production at a good level over the long term, preserving an economic model that enhances its value, and collectively harnessing all the resources at its disposal to consolidate its place in evolving consumption patterns.

The Regional Market: Generous availability eases trade tensions

Although Burgundy has experienced increasingly significant yield fluctuations since 2008, the generous 2023 harvest has raised the average of the last five harvests. However, this average is still below 1.5 million hectoliters.

The production potential changes from year to year, with the total planted area increasing by 12% in 10 years (+3,000 hectares). The harvests of 2021 and 2023 have produced two contrasting situations: -33% in volume for the 2021 vintage and + 29% in volume for 2023 compared to the five- vintage average. These sudden variations seem to have become more pronounced in recent years. As a result, the average of the harvests has hardly changed at all, but the standard deviations have risen sharply.

In addition to these situations, there were two extraordinary and contrasting economic contexts in 2020 and 2021. The first heralded a period of overstocking due to lockdowns, while the second resulted in the 2021- 2022 campaign, with record sales mobilizing large stocks in Burgundy. The less anticipated effects of these two years shaped the 2022-2023 campaign, which saw the confirmation and amplification of new wine consumption patterns driven by younger generations.

The beginning of the 2023-2024 campaign is off to a slow start, awaiting clarification of market trends, both for the French as well as international markets.

In order to balance these increasingly important and regular variables between production and consumption, Burgundy is equipping itself with tools for collectively managing production volumes and marketing.

Vintage 2023: Burgundy demonstrates its potential!

With a production forecast of almost 1.9 million hectoliters2 (equivalent to 253 million bottles), the 2023 harvest demonstrates Burgundy’s considerable production potential, when conditions are favorable.

+9% compared to the 2022 harvest

+29% compared to the average of the last five vintages (2018-2022)

- The 2023 harvest in detail2

- White wines: 1,122,124 hectoliters (+5% compared to 2022)

- Red wines: 518,846 hectoliters (+9% compared to 2022)

- Rosé wines: 5,563 hectoliters (-2% compared to 2022)

- Crémant de Bourgogne: 253,265 hectoliters without reserves (up 32% compared to 2022)

White wines: 59% of this vintage’s volume

- Mâcon Régionale AOCs3 (23% of white volumes produced in 2023): +4.3% compared to 2022

If we include the Village and Village Premier Cru AOCs, white wines from the Mâconnais will account for 34% of the white wines produced in Burgundy in 2023 (up 6.8% from 2022).

- Chablis AOCs4 (31% of white wine volumes in 2023): +19% compared to 2022

Red wines: 27 % of the volumes of this vintage

- Burgundy Régionale AOC (46% of red wine volumes in 2023): +6.4 % compared to 2022

- Burgundy Hautes Côtes de Nuits and Burgundy Hautes Côte de Beaune (13% of red wine volumes in 2023): +7.3% compared to 2022

- Mercurey AOC including the Premier Cru designation (4.8 % of red wine volumes in 2023): +5.5% compared to 2022

Crémant de Burgundy: 13% of the volumes of this vintage

Estate sales: Growth driven by bulk sales of grapes and must

With a generous harvest volume in 2023, estate sales for the first six months of the 2023-2024 campaign have been driven by grape and must sales of the 2023 vintage.

This means that estate sales of bulk wine are up 8% compared to the same period last year, accounting for 67.5% of total sales volumes (bulk + bottles). This strong growth in the bulk format is naturally driven by sales of “grapes and must” from the 2023 vintage:

+14.9% compared to 2022:

- For white wines: +5.8% compared to 2022 (55% of volumes)

- Burgundy AOC: +18.4% for 4% of volumes

- Chablis AOCs: + 2% for 22% of volumes

- Mâcon-Villages AOC: +14.7% for 8% of volumes

- For red wines: +10.6% compared to 2022 (17% of volumes)

- Burgundy AOC: +8.3% for 3% of volumes

- Burgundy Hautes Côtes de Nuits: +10.3% for 3% of volumes

- Mercurey AOC: +13.4% for 5% of volumes

- Crémant de Burgundy (base wine): +40% compared to 2022 (29% of volumes)

As demand is slightly lower than in 2022, sales of bottled estate wine for the first six months of the campaign have declined compared to the same period of the previous campaign: -3.4% (-10.2% for the 2023 campaign compared to the average for the last five campaigns), accounting for 32.5% of total sales volumes (bulk + bottles).

However, some AOCs are making progress:

- Burgundy AOC whites: +4.4%.

- Burgundy AOC reds: +5.6%.

Exports: Market share to be reclaimed thanks to two beautiful vintages, amid a more competitive environment

French wine exports lost almost the equivalent of 190 million bottles in 2023 compared to the average of the last five years. These volume losses reflect smaller and more competitive market shares than in the past.

For 2024, Burgundy will face a number of challenges in terms of exports, because, as in France, wine consumption is evolving in step with the socio-economic context and changing lifestyles, and is becoming more occasional. Over the past ten years, Burgundy has been one of the French winegrowing regions to enjoy steady growth in its exports, while at the same time repositioning its offering in segments that highlight its efforts to enhance the quality of its image and its wines.

In 2023, although the volume of Burgundy wines exported fell (-6% in 2023 compared to 2022), it was still equivalent to the average of the last 10 years (-0.6% in volume compared to the 10-year average), even including the exceptional results of 2021.

Burgundy wines continue to expand their presence around the world: they are now exported to 175 of the 197 countries recognized by the UN (+ 9 new exotic destinations in 20235).

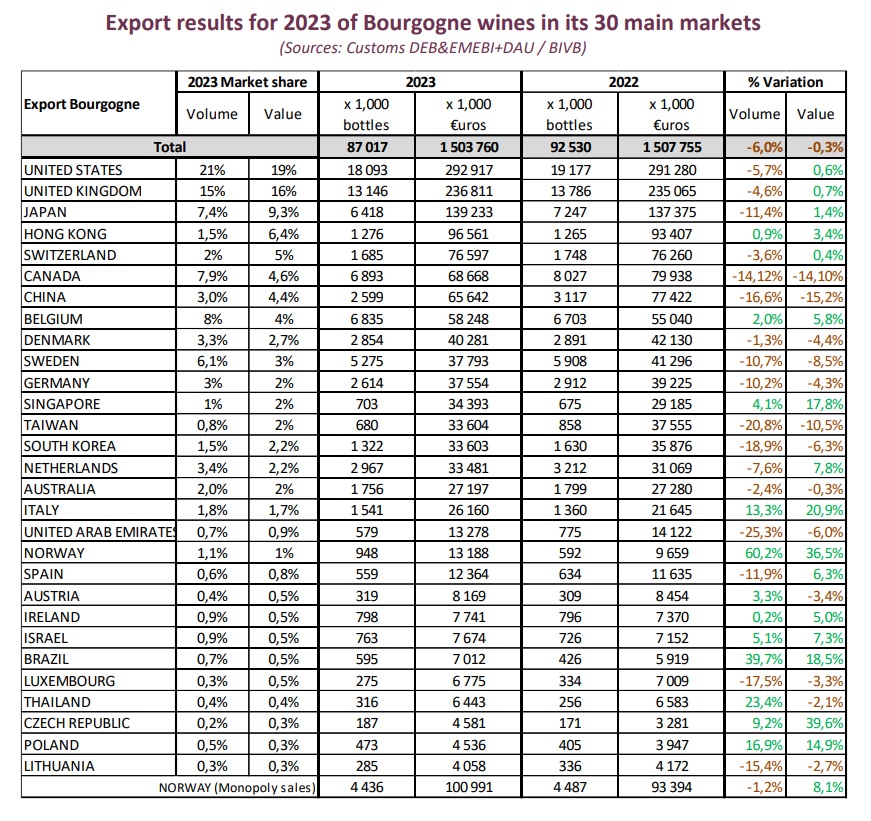

- Burgundy wines sold over 87 million bottles in 2023, equivalent to the export average of the last 10 years.

- Burgundy whites account for 64% of the wine exported by

- Certain high-volume AOCs are regaining market share in 2023: Mâcon Régionale AOCs (+12%, 2023 compared to 2022) and Chablis and Petit Chablis AOCs (+5.2%, 2023 compared to 2022).

- The increase in revenue from white wines in 2023 compared to 2022 (+23.6 million euros, representing 49% of Burgundy’s total revenue) does not, however, offset the decline in red wine

Among white wines, there were excellent performances from Chablis and Petit Chablis AOCs (+15.3 million euros), wines from the Mâconnais AOCs (+14.9 million euros), and Grand Cru AOCs from the Côte d’Or (+9.4 million euros).

- Crémant de Burgundy will account for more than 11% (up 2 percentage points compared to the 5- year average) of all Burgundy wine exports in 2023, with an increase of 2.3% (2023 compared to 2022).

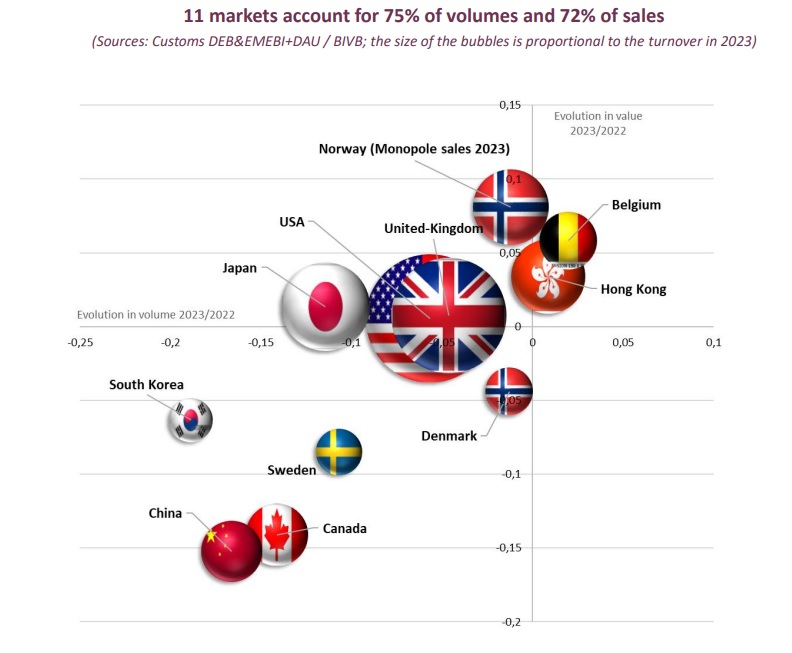

Three main export areas for Burgundy wines

Of the 87 million bottles exported by Burgundy in 2023, most went to three main geographical areas, which together accounted for 75% of volumes and 72% of sales.

- The European geographical area (United Kingdom, Belgium, Sweden, Denmark and Norway) is the largest in terms of volume and sales (33% of volumes generated and 26% of Burgundy’s export sales).

- North America with the United States and Canada, which are in the top three export destinations, being the 1st and 3rd markets respectively in terms of volume: Together they accounted for 29% of volume and 24% of revenue for Burgundy wine exports in 2023.

- Asia (Japan, China, Hong Kong and South Korea) is the fastest-growing region in terms of sales, up 61% on average over the last 10 It accounts for 13% of volumes and 22% of export sales.

Countries in the European geographical area

Burgundy sold 29 million bottles to the area’s five main markets, generating sales of over 386 million euros (down by 0.8 million bottles and up by 3.1 million euros in 2023 compared to 2022).

French wines lost 34.3 million bottles in these countries in 2023 compared to the 5-year average.

- United Kingdom, the 2nd largest market in terms of value (16% of sales, for 15% of volumes) Evolution 2023 compared to 2022: – 6% in volume and +0.7% in value

In 2023, the United Kingdom maintained its position as the 2nd largest export market in terms of volume and value, just behind the USA.

Although export volumes are declining, some AOCs are regaining market share (2023 compared to 2022):

- Mâcon Régionale AOCs in white (including Mâcon-Villages and Mâcon plus geographical designation): +9.4% in volume, accounting for 23% of white wine

- Grand Cru AOCs from the Côte d’Or: a significant increase in volume (+42.7%), accounting for 8% of white wine volumes.

- Crémant de Burgundy: up 1% in volume, accounting for 6.2% of exported volumes. It remains above its 2019 performance.

Sales of red wines and Crémant de Burgundy have risen significantly, by 1.2% and 48.9% respectively (2023 compared to 2022).

Burgundy white wines are very present in this market, and still account for 36.4% of the volume of French AOC white wine exported to the United Kingdom, accounting for 58% of the revenue generated by this category of wine in 2023.

- Belgium, the 8th largest market in value (3.9% of export revenue, representing 8% of volumes) Evolution 2023 compared to 2022: +2% in volume and +5.9% in value

Burgundy white wines still play a dominant role in the export of AOC wines to this country: 29.6% of volumes and 44.5% of sales for this category of wine in 2023. It is these same white wines that show the highest growth in revenue (+4.4 million euros in 2023 compared to 2022).

The turnover generated by Burgundy’s white wines is thus well supported: +12.2% (2023 compared to 2022).

Some very fine performances worth noting:

- Chablis and Petit Chablis AOCs: +23.2% in volume and +36.9% in value compared to 2022

- Mâcon regional AOCs (including Mâcon-Villages and Mâcon plus geographical designation): a +9.6% increase in volume compared to 2022 (30.8% of Burgundy’s white wines) and a +19.5% increase in value (25.6% of sales).

Although Burgundy reds account for only 13.7% of volumes and 26.8% of sales in Belgium, they achieved notable successes in 2023:

- Burgundy regional AOCs (including Burgundy plus geographical denomination): +16.9% in volume (54.1% of exported bottles) and +21.1% in value (20.5% of sales)

- Grand Cru AOCs from the Côte d’Or: + 8 % in volume (just over 6.5 % of exported red wines) and

+10.3 % in value (31 % of sales for this category).

None of these figures take into account direct sales to Belgian tourists. It is worth noting that Belgian tourists are among the most frequent visitors to the Burgundy wine region.

- Denmark, the 9th market in value (2.7% of export sales, accounting for 3% of volumes) Evolution 2023 compared to 2022: -1.3% in volume and -4.4% in value

In 2020, Denmark became one of the top 10 markets for Burgundy wines in terms of value. It confirmed this position in 2023, even overtaking Sweden. In terms of volume, it has held onto its 9th place for over 10 years. Burgundy wines enjoy a strong position, confirming their 2nd place in terms of both volume (2.18 million bottles, representing a market share of 18.6%) and sales (excluding Champagne) among French AOC vineyards.

Burgundy white wines account for 55.6% of export volumes, and 49.4% of total sales. There was a significant increase in volume (+24,000 bottles compared to 2022), driven mainly by:

- Chablis AOCs: up 28.2% in volume compared to 2022 (32.4% of Burgundy white wine volumes) and up 6% in value compared to 2022.

- Burgundy Régionale AOCs (including Burgundy plus geographical designation): +23.4% in volume compared to 2022 (29.4% of Burgundy white wine volumes) and +20.3% in value compared to

For red wines, only the Burgundy Régionale AOCs (including Burgundy plus geographical designation) are experiencing real growth in volume: +4.6% in volume (50.9% of red wine volumes exported).

Crémant de Burgundy, which accounts for 23.5% of volumes, continues to grow: +2.5% in volume and +12.6% in sales.

- Sweden, 10th largest market in value (2.5% of export sales, accounting for 1% of volumes)

Evolution 2023 compared to 2022: -10.7% in volume and -8.5% in value

Despite negative results, Burgundy confirms its 1st place in volume (5.3 million bottles, 23.6% market share) among French AOC vineyards in this market, established in 2018. Burgundy wines rank 2nd in terms of sales (37.8 million euros and 22.2% market share in value) and have held this position for over 10 years, behind Champagne.

This is one of the markets where Crémant de Burgundy is highly exported, with volumes close to those of white wines: 39.9% of Burgundy export volumes for Crémant de Burgundy and 47.7% for white wines. It is also the leading sparkling wine in terms of volume and value exported to this country: 65.8% of the volume and 73.5% of the value of all French sparkling wines excluding Champagne.

Furthermore, Crémant de Burgundy experienced double-digit growth in 2023, both in volume and in value:

+16.5% in volume and +17.8% in sales (2023 compared to 2022).

Burgundy red wines accounted for just 12.3% of export volumes and 19.8% of sales in 2023.

Norway, 7 years of growth for Bourgogne wines

The customs data does not allow us to rank Norway as an export destination for Burgundy wines, as is the case for other destinations, since part of the wine exported to Norway (according to customs sources) transits through other destinations.

However, the figures from the monopoly alone would place Norway as the 7th largest market in volume and 4th largest in value for 2023!

Sales of Burgundy wines by the Vinmonopolet (monopoly) continue to grow over the long term. Although sales in 2023 are slightly down compared to 2022 (-1.2%), they remain higher than the 5-year average: +6.4% in volume and +29.1% in value (2023 compared to the 5-year average).

In 2023, sales of Burgundy wines through Vinmonopolet amounted to 4.435 million equivalent 75 cl bottles (19% of Burgundy wine sales are in the Bag-in-Box format):

- White wines: Only the Burgundy Régionale AOCs (including Burgundy plus geographical designation) saw growth in 2023, up 9% in volume (32.4% of total volume).

- Crémant de Burgundy: Although the AOC experienced a decline in 2023 (-1.3% compared to 2022), export volumes remained above the 5-year average: up by 23% in volume (32% of volumes).

- Red wines: Slightly up (+0.6% in volume) driven by Burgundy Régionale AOCs (including Burgundy plus geographical designation), which account for 3% of the volume of exported red wines from Burgundy.

The monopoly’s revenue from its sales of Burgundy wines in 2023 exceeded 100 million euros (1.15 billion NOK), representing growth of + 8.1% compared to 2022. Red wines showed the strongest growth: +16% compared to 2022. White wines came in second, up 16% compared with 2022, while Crémant followed at +6% compared with 2022.

North America

Exports of Burgundy wines to the USA and Canada totaled the equivalent of 24.9 million bottles, representing sales of 361.5 million euros (-2.2 million bottles and -9.6 million euros in 2023 compared to 2022). French wines have lost 29.7 million bottles on these markets in 2023 compared with the 5-year average.

- United States, the 1st market in value (19% of export sales, accounting for 21% of volumes)

Evolution 2023 compared to 2022: -5.7% in volume and -0.3% in value

In 2023, the United States maintained its position as the leading export market in terms of both volume and sales, ahead of the United Kingdom.

Despite the decline in volume growth, Burgundy whites have regained market share (+2.8% in volume compared to 2022):

- Mâcon Régionale AOCs (including Mâcon-Villages and Mâcon plus geographical denomination):

+28.1% in volume compared to 2022, for 24.8% of white wine volumes, and +42.5% in value compared to 2022.

- Chablis and Petit Chablis AOCs: up 11.2% in volume compared to 2022 (21.7% of Burgundy white wine volumes) and up 4% in value compared to 2022.

- Village and Village Premier Cru AOCs from the Mâconnais: +10.2% in volume compared to 2022 (10.2% of the volume of white wines from Burgundy) and +18.1% in value compared to 2022.

Red wines and Crémant de Burgundy saw a decline in 2023, both in terms of volume and sales.

Burgundy whites, which have a strong presence in this market, still account for 33% of the volume of AOC French white wine exported to the United States, representing 47.8% of the sales in 2023.

- Canada, the 6th largest market in value (4.6% of export sales, representing 9% of volumes)

Evolution 2023 compared to 2022: -14.12% in volume and -14.10% in value

In Canada, Burgundy maintained its position as the top performer in terms of revenue and volume for French AOC still white wines. Despite a drop in volume and value in 2023 (-14.12% in volume and -14.10% in value compared to 2022), Burgundy accounted for 42.3 million euros in revenue, capturing 47.8% of the market share in value.

This leading position is largely attributed to the Chablis and Petit Chablis AOCs, which saw a modest increase in volume (+4.3%) and in value (+6.5%) in 2023 compared to 2022. These appellations accounted for 32.7% of exports by volume and 35.3% of the revenue.

Among Burgundy red wines, only the Village and Village Premier Cru AOCs of the Côte de Nuits showed growth in volume (+3.1%) and in value (+13.8%).

Crémant de Burgundy continued its growth trajectory in 2023, with a 2.3% increase in volume and a 1.8% increase in value, consolidating its position as the second-largest French AOC among sparkling wines in Canada.

Countries in Asia

Within the Asian region, Burgundy wines exported 11.6 million bottles with revenues of 335 million euros across four main markets in 2023. This represents a decrease of 1.6 million bottles and 9 million euros in revenue compared to 2022 for Burgundy wines. French wines as a whole have seen a decline of 63.9 million bottles in these markets in 2023 compared to the five-year average.

- Japan the 3rd largest market in value (9.3% of export sales, accounting for 4% of volumes)

Evolution 2023 compared to 2022: -11.4% in volume and +1.4% in value

Burgundy wines have long held a significant place in French exports of still AOC wines to Japan. In 2023, they maintained their position as the second largest contributor in volume (20.2% of volumes) and the largest contributor in value (46% of the value) among French AOC wines exported to Japan.

Burgundy whites are highly favoured, accounting for 44.5% of the volume of French white AOC wines exported to Japan, and 67.6% of sales in this category.

Despite a drop in the volume exported to Japan, some Burgundy appellations continue to see growth in their sales:

- Burgundy Régionale AOC whites (including Burgundy plus geographical denomination): +7.8% (2022 compared to 2023) representing 2% of white wine sales.

- Chablis AOCs: +5.8% in volume and +9.8% in sales (2023/2022).

- Burgundy Régionale AOC reds (including Burgundy plus geographical denomination): +10% (2022/2023) representing 8% of red wine sales.

Over the past 15 years, sales of Burgundy wines have grown significantly in Japan, increasing by a total of 100% (2023 compared to 2009), driven primarily by Burgundy Régionale AOCs (+48.6 million euros in sales).

- China and Hong Kong the 3rd largest market in terms of value (10.8% of export sales, representing 5% of volumes).

Evolution 2023 compared to 2022: -11.6% in volume and -5% in value.

Whether it’s an anachronistic phenomenon or an emerging trend, white Burgundy wines continue to grow in these two markets, historically driven by red wines (87.7% of French AOC wines exported to these countries are red): +5% in volume (2023 compared to 2022).

Some good results are to be noted (2023/2022), thanks in particular to white wines:

- Chablis and Petit Chablis AOCs: +89% in volume (24.2% of bottles exported) and +71.2% in value (9.9% of sales).

- Village and Village Premier Cru AOCs from the Mâconnais: +0.2% in volume (6% of bottles exported) and +4.9% in value (3.2% of sales).

- Mâcon Régionale AOCs (including Mâcon-Villages and Mâcon plus geographical denomination):

+130% in volume and +56.5% in value.

Red wines, which still account for 55% of Burgundy wines on these markets, experienced a slowdown in 2023, while some AOCs continued to grow in sales:

- Burgundy Régionale AOCs (including Burgundy plus geographical denomination): largely dominant, covering 4% of export volumes and growing in sales (+2.3% compared to 2022).

- Village and Village Premier Cru wines from the Côtes de Nuits: showing significant growth, up 6% in sales.

- Crémant de Burgundy, which is still relatively under-represented (36,000 bottles, representing less than 92% of exported Burgundy wines), achieved a significant double increase: +15.6% in volume and +40.5% in value.

- South Korea is ranked 14th in terms of value (2.2% of export sales, for 5% of volumes).

Evolution in 2023 compared to 2022: -18.9% in volume and -6.3% in value

Since the free trade agreement signed between South Korea and the European Union in 2011, the wine market has seen significant development. In 2021, the volume of French AOC wines reached a new record, surpassing that of 2007 by a large margin. Burgundy wines, which are very popular, are among the French AOCs that have made the most progress.

In 2023, Burgundy confirmed its n°1 position in terms of revenue in 2023 (13.4 million, accounting for 61.2% of market share in value) among the French AOC still white vineyards in South Korea. It has also confirmed its n°1 position in terms of volume, which has not changed for 10 years.

In 2023, the growth of Burgundy wines slowed significantly: -18.9% in volume and -6.3% in value. However, some Burgundy wines continue to progress:

- Grand Cru AOCs of the Côte d’Or in white: +25.3% in volume (3.7% of white wine bottles exported) and +56.9% in value (11.4% of revenue in this category)

- Burgundy Régionale AOCs in white (including Burgundy plus geographical designation): +0.3% in volume (42.4% of white wine bottles exported) and +2.9% in value (32.7% of revenue in this category)

1 all bottles refer to 750 ml bottles.

2 Excluding the VCI (Individual Extra Volume scheme)

3 Mâcon AOCs includes: Mâcon, Mâcon-Villages and the 27 Mâcon plus geographical denomination villages.

4 Chablis AOCs include: Petit Chablis, Chablis (including the designation Premier Cru), and Chablis Grand Cru

5 Zimbabwe, Nicaragua, Djibouti, Guinea, Macedonia, Liberia, Cuba, Namibia, Bhutan, and El Salvador